Every person dreams of someday retiring from their 9-5 job, but retirement is becoming harder and harder to achieve in a world where the monetary system is broken. When the government can print money just as fast or faster than you are earning it in your paycheck and retirement account, you are just “raking leaves in the wind.” Even the “8th wonder of the world,” compound interest, as Warren Buffett describes it, will not save you.

Here is why…

If you invested any amount of money in March of 2020 when the government created 35% of all the money that ever existed, unless you were getting a 35% rate of return on your money, you were and still are raking leaves in the wind.

Bitcoin fixes this!

Here is how just a few fractions of a bitcoin, known as satoshis (1 bitcoin = 100,000,000 satoshis), can help you attain early retirement and accrue Generational Wealth. If you want to fast forward to my calculations below, please do…if not, let me further explain my retirement/generational wealth strategy/ideologies.

Most people think they need one whole bitcoin to become “wealthy.” I place wealth in quotation marks because being wealthy is all relative to one’s definition of wealth. For me, I define wealth as my ability to acquire, earn and attain as much of the following:

- Time with Family

- Health

- Community building

- Skills and Knowledge

- Friends

- Emotional Intelligence

- Helping Others

I highly recommend the book by Adam Taggart and Chris Martenson, “Peak Prosperity,” as it helped me better understand wealth.

So, where does bitcoin stand in my definition of wealth? Bitcoin is #1 because it will allow me to maximize my time with my family through its time preservation properties and ability to appreciate over time faster than inflation. Bitcoin cannot be inflated away like $’s, so every $ I save in bitcoin from my 9-5 job is preserved to its fullest.

Bitcoin to me is like oil was to John D. Rockefeller (JDR). When JDR understood that oil was the energy industry’s future and could standardize it, he knew he would become the wealthiest man in the world. This is why Michael Saylor will be the Rockefeller of this era. When I realized that Bitcoin was once a species’ invention and would be as powerful as Gutenberg’s printing press, I started buying like a madman and could not stop thinking and studying it.

Before bitcoin, I was heavily invested in cash-flowing real estate. My understanding of real estate, monetary history, and gold/silver helped me realize that bitcoin was the best real estate I could ever own because of the following properties:

- Bitcoin is the scarcest, highest-use real estate.

- Bitcoin does not have capital expenditures or deferred maintenance like my properties.

- Bitcoin istaxed like my real estate.

- Bitcoin doesn’t have tenants to deal with

- Bitcoin doesn’t require me to have a maintenance company.

- Bitcoin is highly liquid in comparison to my very illiquid real estate.

- I can refinance my Bitcoin and live off its equity into perpetuity instead of living off the cash flow of my real estate or refinancing my real estate through an arduous, drawn-out process.

As an engineer, I have been engineering my early retirement strategy around real estate for 10+ years through real estate. I would have achieved early retirement by 40 through real estate, but I realized that bitcoin was the best tool and most efficient way for me to engineer my early retirement. More so than early retirement, my bitcoin would be greater generational wealth for hundreds of years in comparison to my depreciating, deteriorating real estate. Real estate is made of materials, and materials break down over time. Bitcoin is made of code and math, which will stand the test of the time forever. As an engineer, this resonated with me and still gives me chills thinking about the much greater efficiencies and qualities of digital scarcity versus physical scarcity.

So, how much bitcoin do you need to attain early retirement and generational wealth? What is Generational Wealth? I define Generational wealth as the ability of my future heirs to spend the wealth I accumulated for them within its appreciation rate. For example, if I earn $100 million dollars for my family and it appreciates at 10% per year, if my heirs spend it at a rate of 20% per year, the wealth I accumulated for them will not last forever.

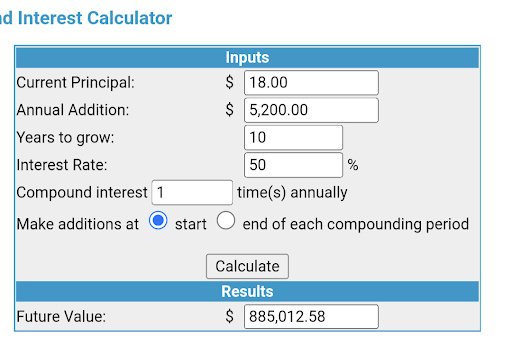

I believe that a person can achieve early retirement by simply owning 0.001 of a bitcoin, $18 worth of bitcoin at today’s value, and saving $10/month for ten years. If you do this for 30+years, you will have generational wealth. Here are the calculations proving this:

Early Retirement Calculation

Scenario = person buys $18 worth of bitcoin and saves $100/week for ten years at a Compound Annual Growth rate of 50%.

Remember, bitcoin’s average CAGR over 13 years has been about 150%, so my calculations are very conservative. (https://finance.yahoo.com/news/compounding-saving-bitcoin-power-dollar-125000227.html)

Run your numbers using the compound interest calculator that I used for my calculations at http://www.moneychimp.com/calculator/compound_interest_calculator.htm

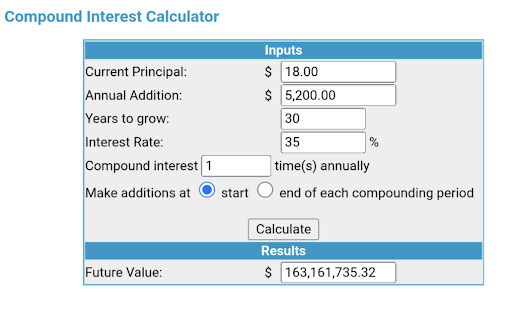

Generational Wealth Calculation

Scenario = Person buys $18 worth of bitcoin and saves $100/week for 30 years at a Compound Annual Growth rate of 35%.

I use a 35% CAGR in this calculation because I do not believe that a 50% CAGR is sustainable over a 30 year timeframe.

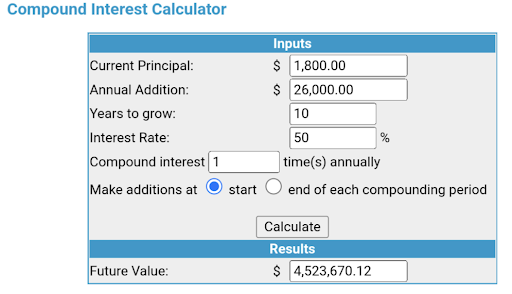

For those of you who can save $500 per week, can afford 0.1 bitcoin ($1800) and need a higher annual income in retirement to live, here are some calculations for you:

Early Retirement Calculation

Scenario = Person buys $1800 worth of bitcoin and saves $500/week for 10 years at a Compound Annual Growth rate of 50%.

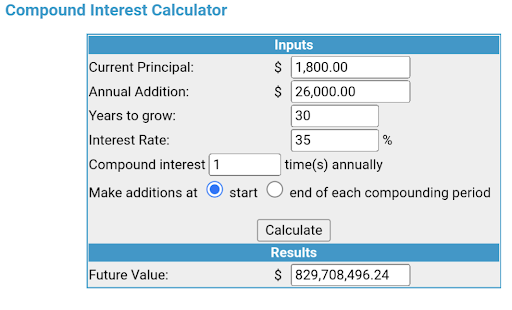

Generational Wealth Calculation

Scenario = Person buys $1800 worth of bitcoin and saves $500/week for 30 years at a Compound Annual Growth rate of 35%.

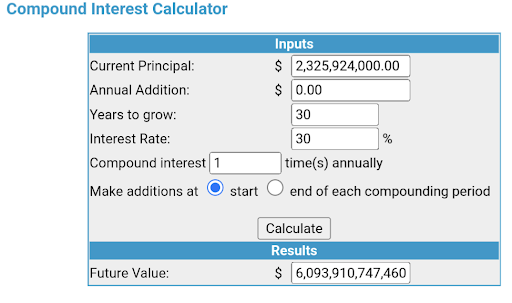

If you can become close to a billionaire owning just 0.1 bitcoin, imagine Michael Saylor’s compound interest calculations owning ~129,218 Bitcoin! Instead of imagining, here they are:

Michael Saylor’s Generational Wealth Calculation

Scenario = Saylor lets his ~129,218 worth of bitcoin (calculated at today’s market price of about $18000/coin) grow for 30 years at a Compound Annual Growth rate of 30% without buying anymore.

Yes, he will be a trillionaire and second only to Satoshi Nakamoto.

Conclusion

Now that you know what $18 (0.001 bitcoin) and $1800 (0.1 bitcoin) worth of bitcoin can do for you, I hope you are consoled by the fact that you don’t need to own one whole bitcoin to attain generational wealth. I implore you to possess as much bitcoin as possible, all within your purchasing power and the responsible use thereof.

I will leave you with one last analogy for why I believe bitcoin will be generational wealth for my family. Have you ever been to a 100-year-old fruit orchard? Have you ever wondered who the person was that planted it and their motives? I have visited a 100 year plus olive orchard and have thought about these things and know without a doubt in my mind that the person that planted those seedlings or seeds 100 years ago did not grow them for him/herself. They produced the orchard, tended to it, and nurtured it for their heirs to enjoy the fruit, shade, and beauty. They also planted them to provide sustenance for as many people as possible.

I am doing the same for my family. I am planting as many seeds (satoshi’s) in my family’s orchard, tending to them and nurturing them so that my family and many people will enjoy the fruits of my labor. Luckily with bitcoin, as opposed to trees, I can enjoy some fruits of my labor within the next five years because bitcoin can grow faster than a tree. Someday your family will also be able to enjoy the fruits of your labor based on your purchase of as much as 100,000 satoshis (0.001 bitcoin).

Keep on stackin sats because every satoshi counts.

This is a guest post by Jeremy Garcia. You can follor him on Twitter @jerimican5445. Opinions expressed are entirely their own and do not necessarily reflect those of Satoshi’s Journal or Satoshi’s Entertainment Company.