How does the saying go? Fool me once, …shame on me, fool me twice… Ok, my fellow workers, in this edition of Proof of Workforce, we explore time and money.

FOOL ME ONCE

As workers, we trade time for money. Whether that is a good transaction or not depends on endless circumstances. We both sell and buy our time. Just finishing a shift at the hospital? You sold your time for money. But too tired to cook dinner? You just paid for that DoorDash delivery to buy time. At the end of the day what is most important is this: if you ARE going to trade time for money, you’d better make sure your money holds over time.

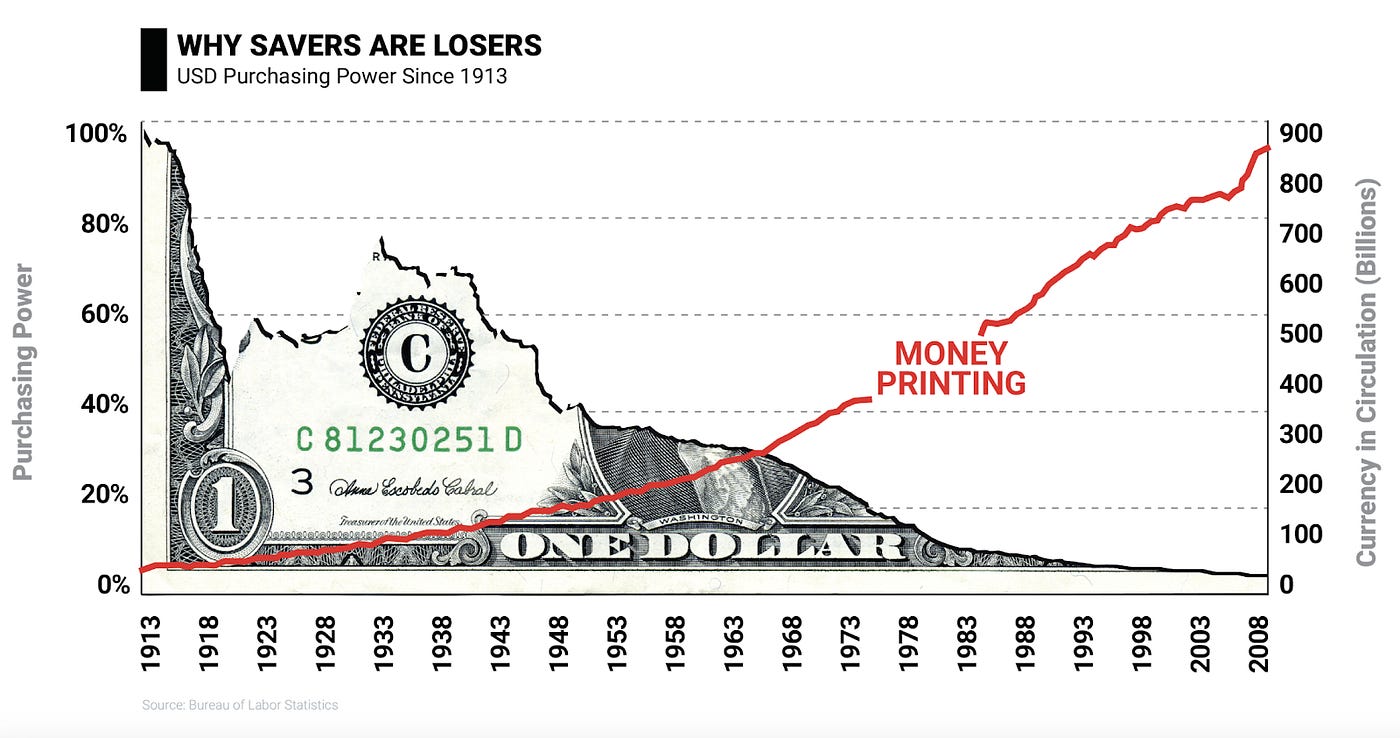

Other than a brief period of deflation in the late 1920’s/early 30’s, the purchasing power of the dollar has steadily decreased. As workers, we trade our time for money that loses purchasing power even as you read this.

The numbers don’t lie.

In the short term, workers are beat up by inflation. Killed. Long term, our pensions, retirement funds and social security will face many challenges (and we’ll get to that in the “Fool Me Twice” section).

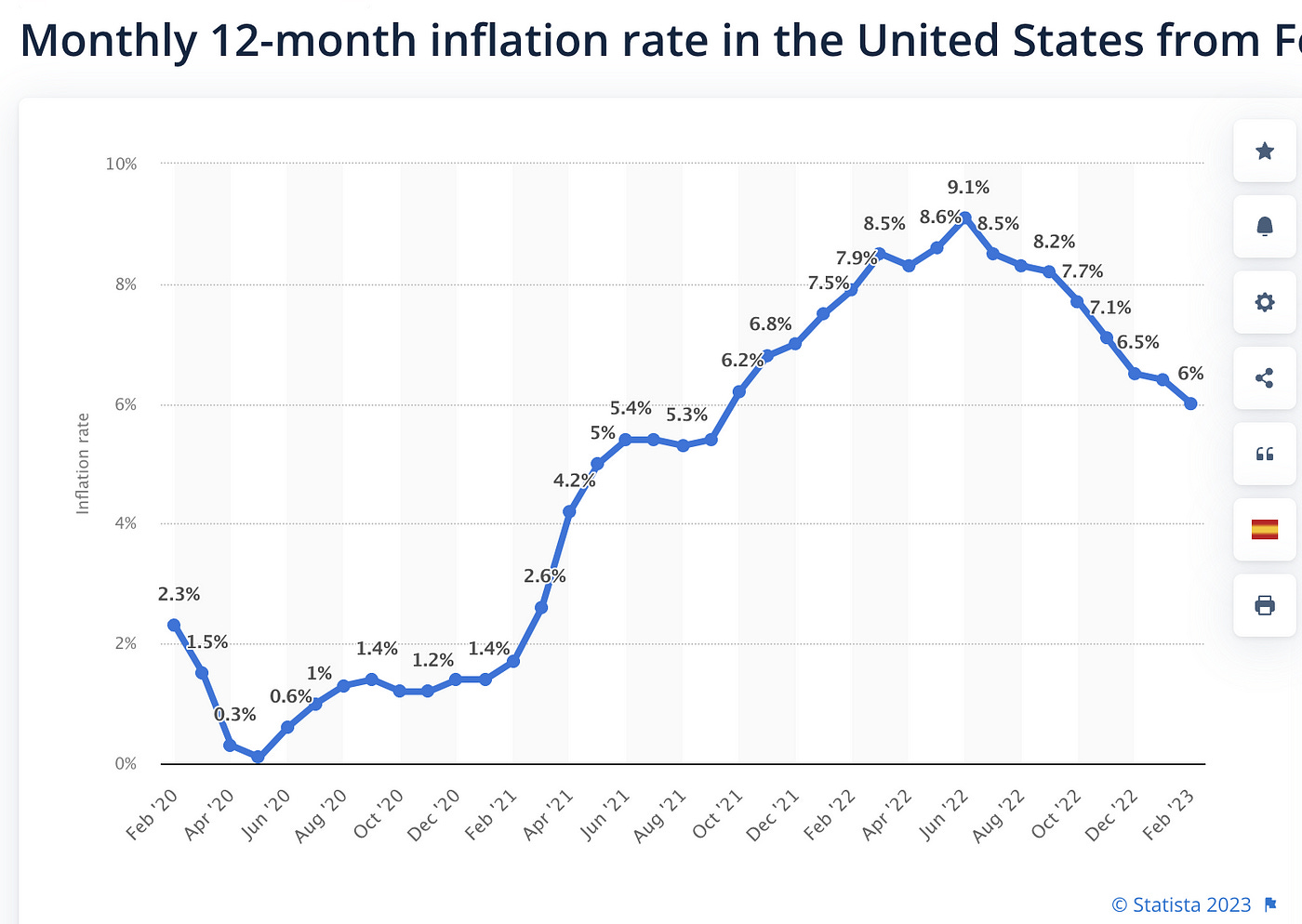

Inflation is like time card theft. It’s important to note that in the second chart (above), inflation going down month to month is not deflation, or the dollar re-gaining strength, it’s simply a lesser version of higher costs. And at the end of the year, monthly inflation percentages are averaged for that year. In 2022, the average CPI inflation percentage was 8 percent. That’s excluding housing and energy, two of the most expensive living expenses. If the latter were included, real inflation is actually much higher. At minimum, did you get an 8% raise in 2022? If not, very conservatively, you took a pay cut of the difference, if not more. You traded time for money that did not hold its value over time.

“But didn’t Bitcoin, like, go down a bunch?”

(Bitcoin vs. Dollar: Zoom Out)

The most common opposition to Bitcoin I hear is: “Wasn’t Bitcoin just at 70k a coin or something before it dropped to like, 15k a coin?”. Those who refuse to learn about Bitcoin seem hyper focused on this point, and take Bitcoin’s recent drop as an opportunity to dismiss it. This is short term thinking, aka high time preference…meaning, this is from a view point of prioritizing present gratification over future needs.

This is ironic for workers, many of whom trade a lifetime of work for a guaranteed pension or 401k at the end of their careers. With this mindset, why do workers not pull out of their pensions or 401ks after setbacks? Pensions took massive hits after the 2008 Financial Crisis. They took further hits from the Covid-19 pandemic and recent banking failures. Future setbacks loom on the horizon, including a pending commercial real estate crisis, sluggish city/state revenues, and poor performance of equities and bonds, all of which can come together to cause pension collapse.

But if I get paid in Bitcoin, what if it drops drastically; aren’t I trading time for money that doesn’t hold up in the short term? Yes. But we are talking very short term. Consider this. Bitcoin has gone up steadily over its 14-year lifespan. And in the big picture, while the future of digital money is only in its infancy, it is growing up fast. As the legacy financial system becomes more fragile over time, Bitcoin becomes stronger and more stable every day. On the contrary, doesn’t it feel as if the current financial system is always being “rescued” or bailed out?

Bitcoin’s open source nature and fixed supply mean that people around the world are contributing improvements and building new applications, without sacrificing Bitcoin’s integrity. One such application, Strike, allows workers to be paid in Bitcoin, pay immediate expenses in dollars, and save in Bitcoin; thus reaping the benefits of Bitcoin’s rising purchasing power. Those who remain in the legacy financial system will continue to be the scapegoat for its shortcomings. The near and long term losses of purchasing power will make short term Bitcoin fluctuations pale in comparison.

FOOL ME TWICE

A worker’s career is a marathon not a sprint, and retirement is the finish line. In the past, if you played the long game, some of your short term losses to inflation would be balanced by long term gains. While this doesn’t negate trading time for money that doesn’t hold over time, we keep our heads down knowing we have a pension or 401k at the end of our career. This in addition to Social Security, all with cost of living increases built in.

Let’s take a look at that pot of gold at the end of the rainbow. Here’s a message from CalPERS, The California Public Employees Retirement System, the largest Pension in the United States of America:

“ We’re an estimated 81.2% funded as of June 30, 2021. Our estimated funded status for June 30, 2022, is 72%. This is a measure of the fund’s financial status when comparing the assets to the liabilities.”

This means that the largest pension fund in the nation, as of June 2022, has 72% of the money it needs to fulfill its obligation to those collecting pensions and slated to collect pensions. The difference can only be made up through consecutive years of significant returns from investments, increased contributions from participating cities (i.e., the city’s taxpayers), or increased contributions from workers.

In the past decade, it’s been the taxpayers and employees who have had to make up the difference. Despite these efforts, and in addition to sweeping pension reform initiated in 2013 that required more contributions from employees and longer years of service, the funded status remains at 72%. This is while entering a potentially turbulent economic time ahead. Lastly, CalPERS has demonstrated a more cautious stance after the bludgeoning of 2008–2009. They had high hopes as the fund recently tried their hand at VC investing, earning a meager .5% annual return. While VC ventures take years for realized returns, unless CalPERS engages in truly emerging innovation, it will unlikely ever return to 100% funded.

Social Security is a similar story:

“As a result of changes to Social Security enacted in 1983, benefits are now expected to be payable in full on a timely basis until 2037, when the trust fund reserves are projected to become exhausted”

Social Security is another pillar of the legacy financial system, a system on the tail end of its lifespan. The above statement isn’t from CBS or Fox News. This is directly from the Social Security Office.

Imagine this: Let’s say your entire family, immediate and extended, made a deal with another family to mow that family’s lawn every day for a month in exchange for all the fruit from their fruit trees that month. Then imagine you saw them chopping down their fruit trees each day. Would you still mow the lawn? Knowing that eventually your family would be mowing lawns for nothing? Of course not.

But what if the trees were hidden behind a curtain while being cut down each day?

In that case, you would just show up at the end of the month, and ask for what was promised, only to find out it wasn’t there. Following the 2008/09 crisis, the massive setbacks from Covid, and mechanisms that have been in place for decades, this is how the legacy financial world has been operating. They are moving pieces around and borrowing from behind a curtain. They have to. And you are still mowing lawns naively, unaware. Even if your stance is a refusal to learn about Bitcoin, I’m asking you to at least look behind the curtain.

Fooled Me Twice: Now What

You may have just come to the realization you are getting smoked both in the short term (in diminished purchasing power of the US dollar against long term inflation, with no return in site), and in the long term ( a pension facing massive challenges ahead that can only be made up with incredible returns that defy recent investment trends, coupled with paying more money out of your pocket in contributions into a failing investment). If that’s the case, then you are at least open to exploring Bitcoin.

In my next installment, I will lay out a simple plan for unions and their members to responsibly enter the world of Bitcoin. But, in the meantime, here are three simple actions to consider:

1. Provide access to reliable and trusted Bitcoin education for workers (internal or externally sourced)

2. Run and operate a Bitcoin Node (a great way to support a thriving network, provide a decentralized payment portal to the workforce, all while learning about Bitcoin at little to no cost)

3. Evaluate what Bitcoin would look like on your balance sheet and why it could be an important long term benefit for the workforce

To wait on the sidelines of an emerging innovation is understandable. However, failing to learn about one of the most innovative financial tools of our time is a failure to protect the incredibly valuable time of our workforce.

Stay tuned.

Vires in Numeris,

Dom Bei

About the Author: Dom Bei is an active firefighter with 10 years of elected union leadership having held the positions of Director of Political Action, Vice-President, and President of the Santa Monica Firefighters.

Financial Disclaimer: This is not financial advice. All individuals and financial fiduciaries are encouraged to verify any pertinent information and perform their own due diligence.